If you’ve been reading my blog you’d know that I think Roth savings are a great opportunity for many, many investors. If you plan to max out your contributions this year you can effective save more by saving in a Roth, whether an IRA or 401(k). Recently I’ve run across a common calculator available on the internet. When a user puts in their details it is supposed to help you compare saving in a Roth 401(k) or traditional 401(k). However, the default assumption is that when you decide how much to contribute you will reduce the amount you will be saving in a Roth by the amount of taxes you would have to pay. That seems like something a rational investor would do, right? She would calculate the after-tax expected return of each and make a decision. The truth is that is just not how people operate. After years of providing advice and doing my best for my clients, I’ve never had one say to me, “if I’m going to write a check now to my IRA I can write 20% more if it’s into my traditional IRA than my Roth.” Instead, it’s, “I have $4,000 saved up from my budget. What’s the best I can do with this?”

If you reduce the amount you’d save into a Roth account by your effective tax rate and your tax rate stays the same when you take it out and the investment returns are the same then it doesn’t make a difference whether you save in a Roth account for a traditional account. An investor walks away from that thinking, no big deal, this doesn’t matter. But what they miss is the increased flexibility with Roth savings, the benefit of not having to take required minimum distributions (RMDs) starting at 70-and-a-half, and that they can effectively save more if they’re planning on contributing the maximum amount. Let’s look at that last point. If you contribute the maximum amount to a Roth IRA this year, $5,500 if you’re under 50, then all of that investment will go tax free and an investor will never pay taxes on the gains. If you contribute $5,500 into a traditional IRA any taxes on your contribution and gains are deferred and will be taxed at distribution. Just looking at those two wouldn’t be fair, since you paid tax already on the Roth but not the traditional the Roth is significantly better. To make the case fair you’d have to assume that the tax savings you received from contributing to a traditional IRA were also saved in an individual investment account (this rarely happens). If that account achieved the same returns as the traditional IRA it would still result in a lower after-tax return because there is no deferral on realized gains. That small amount of incremental taxation or tax drag makes the Roth IRA a superior investment simply because none of the saved amount experiences the tax drag.

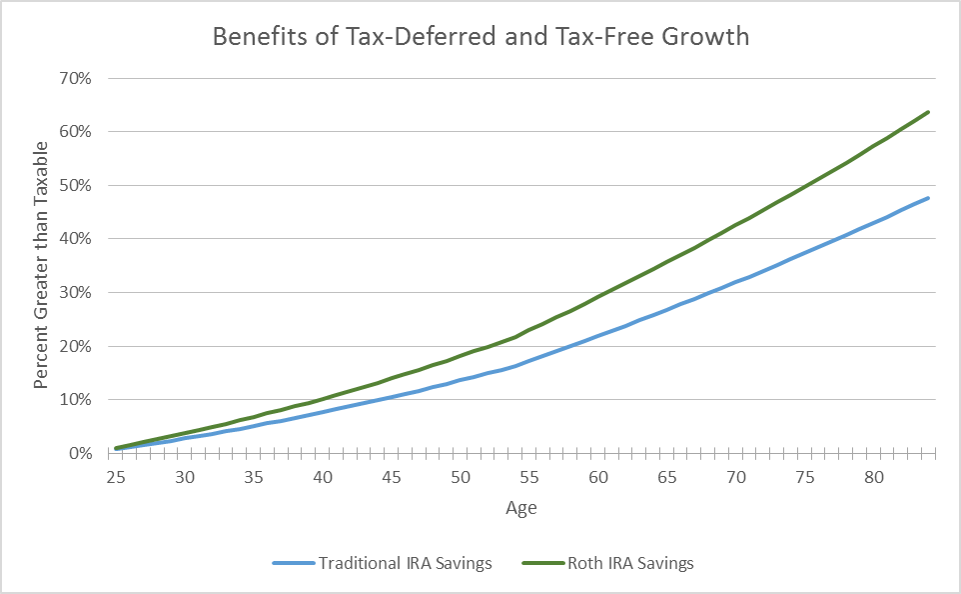

Assumptions: 25% tax bracket, contribute $5k per year Jan 1 starting at 25 for 30 years. Compounded growth at 7% for tax-advantaged accounts and 15% less at 5.95% for taxable accounts. Tax savings from traditional is invested and earns a 5.95% return. Percentage calculated is net of taxes paid on the deferred investment.

Now I want you to think the last time you made a decision to invest in something based on the tax consequences. It is a good thing for an investor to consider after-tax returns and net income in every situation but it is also important to understand the magnitude of tax concerns compared to other considerations. A good financial advisor should be aware of that and help you to make wise choices regarding after-tax returns among the all of the investor’s other financial goals. So the next time you run across a fancy looking internet calculator think twice before thinking it applies directly to you.