Introduction

As asset managers, our primary focus often centers on optimizing investment portfolios to generate returns. Yet, in the broader context of wealth management, it's crucial to consider the entire financial landscape of our clients. Cash reserves play a significant role in this equation. Many investors, including retirees, maintain cash reserves for short-term liquidity needs, comfort, and security. These cash holdings ensure that everyday expenses can be met, safeguarding short-term lifestyle needs, while investment portfolios work toward long-term wealth accumulation. However, the presence of substantial cash holdings can lead to a "cash drag" on long-term returns. In this article, we explore a concept called "return stacking" that offers a potential solution to this conundrum, allowing investors to harness the full potential of their wealth.

Case Study: Cash Reserves in Retirement

Retirement is a life-altering phase, promising newfound freedom and leisure. However, from a wealth management perspective, ensuring financial security in retirement requires balancing short-term comfort with long-term sustainability. Retirees often opt to maintain a portion of their wealth in cash, serving as a financial cushion for immediate expenses. This strategy offers peace of mind, providing retirees with a clear view of their financial situation and a means to cover unforeseen expenditures.

Nevertheless, this approach forces retirees to make a choice: either consistently diminish their investment portfolio to maintain a substantial cash buffer or keep cash reserves to a minimum, relying on investments to support their retirement. The article argues that this doesn't need to be an "either/or" scenario; it can be an "and." Return stacking provides a solution that allows investors to hold significant cash reserves while maintaining a fully invested wealth allocation.

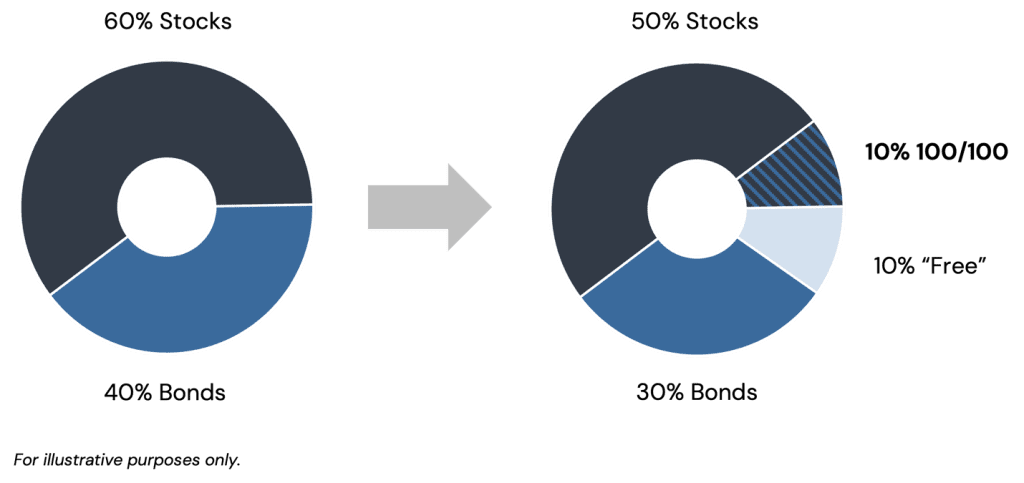

How Return Stacking Changes the Conversation

At the core of the return stacking concept is a simple mathematical equation. The expected return of an entire wealth portfolio (E[Rw]) can be calculated as a weighted average of the expected return of cash (E[Rc]) and the expected return of the investment portfolio (E[Rp]), where the weight is the allocation to cash (c). The equation reads: E[Rw] = c x E[Rc] + (1 – c) x E[Rp].

Return stacking introduces a game-changing notion: what if investors could remain fully invested while accessing a line of credit at an extremely low interest rate, with interest payments automatically deducted from investment returns when the credit is used? This approach essentially enables investors to borrow cash to augment their investment portfolio without liquidating existing holdings.

In this new framework, investors can add back the same percentage they allocate to cash into their investment portfolio. As a result, the cash drag on their wealth is eliminated. The equation with return stacking reads: E[Rw] = c x E[Rc] + (1 – c) x E[Rp] + c x (E[Rp] – E[Rc]). Simplified, this equation yields the same return as the investment portfolio alone: E[Rw] = E[Rp].

In practical terms, if an investor allocates 10% of their wealth to cash, they can employ return stacking to increase their investment portfolio by 10%, effectively offsetting the cash drag.

Two essential considerations are highlighted. Firstly, return stacking assumes that the return on cash (E[Rc]) is similar to the implicit borrowing cost for leverage within the return stacking process. Secondly, investors can choose when and how to repay the borrowing, giving them flexibility in managing their leverage.

How to Implement Return Stacking

Implementing return stacking involves reallocating a portion of the cash allocation to enhance the investment portfolio. For example, in a fund where each dollar invested provides exposure to both equities and bonds, an investor can sell a fraction of their stock and bond positions, using the proceeds to buy a corresponding portion in the fund. This approach releases cash that remains safely in the bank while keeping the investment portfolio fully invested.

The critical advantage of return stacking is that it provides investors with an efficient way to right-size their investment portfolio without liquidating assets. It is akin to borrowing cash for additional investments while having the option to repay the borrowing according to their needs.

How Would This Have Helped?

A backtest of return stacking was conducted in a scenario where investors retained 10% of their wealth in cash, regularly adjusting to maintain this allocation. The investment portfolio was diversified across stocks, bonds, and managed futures, with periodic rebalancing. This approach allowed for a comparison between portfolios with and without cash drag.

The results reveal that, as expected, the total wealth of the investor without return stacking lagged behind that of the investment portfolio due to the 10% cash allocation. With return stacking, the total wealth grew in line with the investment portfolio. This outcome demonstrates that return stacking successfully eliminates the cash drag on wealth.

Conclusion

The concept of return stacking presents a compelling solution to the issue of cash drag on investment portfolios. Investors can now hold substantial cash reserves for short-term liquidity needs and maintain a fully invested wealth allocation. This approach ensures that both short-term financial security and long-term wealth accumulation are achievable. The backtest demonstrates that return stacking effectively mitigates the negative impact of cash drag.

Return stacking introduces flexibility, enabling investors to adapt their leverage to their unique needs and financial conditions. This approach encourages investors to harness the full potential of their wealth without being constrained by the presence of cash reserves.

In summary, return stacking transforms the conversation about managing cash and investments. It offers a way to reconcile short-term liquidity needs with long-term wealth goals, providing investors with a powerful tool to maximize returns and achieve their financial objectives.

This article is a summary of https://returnstacked.com/cash-drag-liquidity-needs-and-return-stacking/ additionally, pictures and graphs are from that site.