RMD stands for required minimum distribution. With some exceptions, when you turn 72, the IRS requires that you start taking money out of your 401(k), 403(b), 457(b), profit sharing plans, Traditional IRA, SIMPLE IRA, or SEP IRA. How much money you must take out depends on your age, your account beneficiary, and your account beneficiary’s age(s). Most people use the Uniform Lifetime Table (scroll halfway down) to calculate their RMD. This table applies to the following people:

· All unmarried retirement account owners.

· Married owners whose spouses are close in age (less than 10 years age difference).

· Married owners whose spouses aren’t the sole beneficiary of their retirement account.

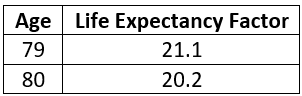

Here is part of the Uniform Lifetime Table. Let’s work through an example with Jim, a retiree.

Let’s say Jim turns 79 in 2022. You calculate an RMD by looking at the account value on December 31, 2021. You divide that number by the Life Expectancy Factor. So if Jim’s Traditional IRA account has a balance of $125,000 on December 31, 2021, his 2022 RMD is $125,000 / 21.1 = $5,924.17. This RMD must be distributed by December 31, 2022. As people age, their Life Expectancy Factor decreases.

RMDs are subject to taxes if they come from traditional (pre-tax) retirement accounts. Roth 401(k)s, Roth 403(b)s, and Roth 457s distributions will not be taxed (assuming you are older than 59.5), but they still must distribute according to the RMD schedule. Only Roth IRAs are exempt from RMDs. For this reason, we recommend rolling any employer-sponsored Roth plans into your Roth IRA at retirement.

Now there is two exceptions to the dates required for RMDs. Clara will be our example person here.

1) The year in which you turn 72 (the first required year for an RMD), you don’t have to take your first RMD until April 1 of the following year. So if Clara turns 72 in 2022, she doesn’t need to take her first RMD until April 1, 2023. But the account balance on which the RMD is calculated is from December 31, 2021.

2) Account owners of 401(k), profit-sharing, 403(b), and other defined contribution plans have the option of postponing their RMDs until the later of age 72 or retirement. Let’s say Bob works for a company and retires in June 2022 at age 75. He wasn’t required to take RMDs from his 401(k) in the past because the company employed him. He must take his first RMD (2022) by April 1, 2023. All subsequent RMDs must be taken in the calendar year for which they apply. So his 2023 RMD must be taken by December, 31 2023.

What if I am married, but my spouse isn’t the beneficiary of my IRA?

You would follow RMDs with a different table. It’s called Table 1 (Single Life Expectancy). Generally, the Life Expectancy Factor is smaller, which means the RMD distribution is larger. Here is part of Table 1.

Let’s look at Jim again. Jim turns 79 in 2022 and has $125,000 in his IRA on December 31, 2021. If he is married, but his spouse isn’t a beneficiary of his IRA, Jim’s 2022 RMD is $125,000 / 11.9 = $10,504.20. This is about double the RMD if his beneficiary was his spouse. Generally speaking, the IRS is trying to de-incentivize passing and IRA onto younger generations. They want their taxes now.

What if my spouse is the sole beneficiary, but he/she is more than 10 years younger than me?

You follow RMDs from a third separate table (this is the last one – I promise). It’s called (creatively) Table 2 (Joint and Life Last Survivor Expectancy) – Scroll about 75% down. Let’s say Jim turns 79 in 2022 and his wife turns 67. Just as before, Jim’s IRA value is $125,000. But the Life Expectancy Factor is 22.5 (see below). Jim’s RMD is $125,000 / 22.5 = $5,555.55.

You can see that, for Jim’s given age, the younger the spouse, the larger the factor, and thus the smaller the RMD. The IRS is recognizing that the IRA will need to last longer to support the younger spouse. RMDs in this situation are less than the RMDs for the Uniform Lifetime Table for the same account holder age.

What if I inherited a retirement account from someone? Do I need to take RMDs?

These rules get a little tricky. We are going to post a blog post about these in the future. Stay tuned.

Is there any way to avoid taking RMDs?

Generally, you need to take RMDs. But there are two ways to work around them for some people.

1) If you have investments in an employer-sponsored Roth plan (Roth 401(k), 403(b), 457), you can roll this over to a Roth IRA. Roth IRAs don’t have RMD requirements.

2) If you are charitably inclined, you can do a qualified charitable distribution (QCD). Basically, you send what would have been your RMD to a charity (non-profit organization) directly from your retirement account. A QCD isn’t taxed and the RMD requirement is waived. If you already give to a non-profit, a QCD is a better way to give than direct cash for two reasons.

a. It gives you the same tax advantages of donating to charity without having to itemize your deductions.

b. Satisfies your RMD requirement.

If you have questions about RMDs, give us a call at 571-969-1459 or email us at ryan@ifpinvest.com.